Real estate continues to be one of the most sought-after methods for building and preserving wealth in the United States. Whether you’re buying your first home or expanding your real estate investment portfolio, understanding your funding options is crucial to achieving long-term financial success. In this guide, we’ll break down the most popular real estate funding sources for 2025, highlighting the pros and cons of each to help you make informed decisions.

Key Takeaways: Understanding the Top Funding Sources

- Conventional bank loans are common for homeowners but less favorable for investment properties due to stricter requirements.

- Home Equity Lines of Credit (HELOCs) offer access to capital but come with significant risks if payments aren’t made on time.

- Private money loans provide flexibility but depend heavily on personal relationships and are unregulated by financial institutions.

- Seller financing offers creative, flexible terms but carries risks such as higher interest rates and potential financial complications.

- Cash financing is the fastest and most straightforward option but requires significant upfront capital.

Conventional Bank Loans: A Reliable Funding Option for Real Estate Investors

Conventional bank loans are the go-to financing option for homeowners. These loans typically offer low down payments (as little as 3% for eligible borrowers with a credit score of 620 or higher). However, when it comes to investment properties, conventional bank loans are less favorable. Lenders typically require a down payment of at least 20-30% for investment properties, and they also impose higher interest rates and stricter credit score requirements. Although the repayment period for conventional loans can range from 15 to 30 years, the efficiency of this funding method is largely determined by the borrower’s financial profile, including credit score, income, and debt-to-income ratio (DTI).

Home Equity Line of Credit (HELOC): Tapping into Home Equity Funding

If you have equity in your current property, a Home Equity Line of Credit (HELOC) may be an appealing option. A HELOC allows you to borrow up to 80% of your home’s equity, providing funds that can be used for down payments, property renovations, or repairs. The advantage of HELOCs is that they typically offer lower interest rates than other types of loans, and the funds are available as a revolving line of credit, similar to a credit card. However, because your home serves as collateral, failing to repay the loan can result in foreclosure. Additionally, HELOC interest rates can fluctuate, which may add uncertainty to your repayment costs.

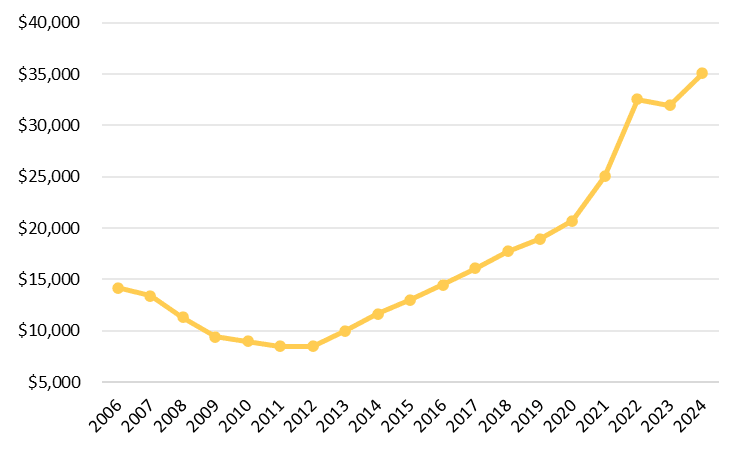

U.S. Households’ Equity (in $USD billions)

Note: Chart shows Federal Reserve Bank of St. Louis’ U.S. Households; Owner’s Equity in Real Estate from 2006-2024

Hard Money Loans: A Fast-Track Funding Option for Real Estate Investors

Hard money loans are a popular option for real estate investors who need quick access to funds for property renovations. These short-term loans are typically provided by private lenders or investors and are based primarily on the value of the property being purchased, rather than the borrower’s credit history. One of the key advantages of hard money loans is their speed – they can be funded in as little as a few days. However, this convenience comes with a high cost. Interest rates often range from 10-18% or higher, and hard money loans also come with fees such as origination and closing costs. Due to their high rates, hard money loans are best suited for investors who plan to quickly renovate a property and refinance it with a conventional loan or another funding option.

Private Money: Unlocking Alternative Funding for Your Real Estate Ventures

Private money loans are loans provided by private individuals or companies rather than banks. These loans are often issued to family, friends, or personal contacts who seek to generate profit from interest. Private loans offer flexibility in terms of loan amounts, repayment schedules, and interest rates, but they can vary widely based on the lender’s preferences. One key advantage of private money loans is the lenient approval process, as they don’t rely on credit scores or institutional underwriting. However, investors should be cautious about mixing personal relationships with financial agreements, as the terms aren’t regulated by financial institutions and could potentially strain relationships if the loan isn’t repaid on time.

Seller Financing: A Creative Funding Solution for Real Estate Investors

Seller financing, or owner financing, occurs when the property seller directly finances the purchase for the buyer. This funding option allows for flexible terms and can expedite the transaction process. Typically, the seller sets the loan terms, including the interest rate and repayment schedule, which can often be more favorable than those offered by traditional lenders. This can be especially appealing to investors looking to avoid banks and streamline the buying process. However, seller financing carries risks: higher interest rates are common, and if title insurance is not obtained, the property may come with hidden financial issues, such as outstanding liens or taxes, which the buyer would be responsible for repaying.

Cash Financing: The Fastest Route to Real Estate Investment Capital

For investors with immediate access to funds, cash financing is the simplest and quickest way to purchase real estate. By using cash, investors avoid the complexity and costs of securing a loan, including interest payments, lengthy approval processes, and closing fees. Cash transactions also tend to close faster, often giving investors a competitive edge in bidding wars, as sellers typically prefer cash offers due to the certainty and speed of the deal. While cash financing requires substantial upfront capital, it eliminates the need for monthly loan payments, allowing investors to fully own the property from day one.

Bottom Line

Choosing the right funding option for your real estate investments is a critical decision that can significantly impact your success. Each option—whether it’s conventional bank loans, HELOCs, hard money loans, private money, seller financing, or cash financing—has its own set of advantages and challenges. By understanding the features and costs of each funding source, you can select the option that best aligns with your financial situation, investment strategy, and risk tolerance. Ultimately, the right choice can turn your real estate endeavors into profitable ventures while minimizing financial risks.

How Turn Edge Estates Property Solutions Can Help You with All-Cash Real Estate Closings in Charlotte North Carolina

At Turn Edge Estates, we simplify the property acquisition process by offering cash for properties, streamlining the investment journey. We provide fast, hassle-free transactions that bypass traditional financing hurdles. Our cash offers help investors and homeowners alike close deals quickly, avoid lengthy approval processes, and move forward with confidence.